If you audited a manufacturing plant and found it occupied 77% of the floor space to produce only 18% of the inventory, you wouldn't call it a business. You would call it a design failure. In our global food system, that is exactly the architecture we have inherited. Livestock, including grazing land and the crops grown to feed animals, occupies 77% of all global agricultural land while producing just 18% of the world's calories. That figure comes from Poore and Nemecek's 2018 meta-analysis, covering 38,000 farms across 119 countries. Even when excluding rangeland unsuitable for cropping, livestock still occupies 40-50% of high-quality arable land while producing the same fraction of calories. The inefficiency persists at every layer of analysis.

Three-quarters of agricultural capacity. Less than a fifth of food output.

I’ve spent fifteen years building capital-intensive infrastructure, first in the federal government, where I led the consolidation of hundreds of data centers and co-authored the commercial frameworks that made cloud adoption viable for risk-averse institutions. Then, at AWS, where I led international expansion, bringing hyperscale data centers to new countries, including a first-of-its-kind disaster recovery architecture in Japan, years before demand certainty existed. I also launched AWS Wavelength, a global 5G edge computing platform, turning telco carrier rivalries into partnerships that brought distributed computing to new markets. Most recently, I designed commercial and pricing frameworks that enable leading AI model providers to scale their training and inference clusters on AWS. I’ve learned that when a system hits a physical ceiling, you don’t just optimize the old hardware. You also rethink and build a new stack. That’s why I am here.

Part One: The Food Security Imperative

By 2050, there will be nearly 10 billion people on this planet. Global meat demand is projected to rise to 455 million tons, a 43% increase over 2016 levels. Meanwhile, per capita cropland has already shrunk from 0.42 hectares in 1960 to 0.20 hectares today, a drop of more than half, according to FAO's 2024 land statistics, and is projected to fall further to ~0.15 hectares by 2050 as population growth outpaces any plausible expansion of arable area. A system that produces less protein per unit of land, deployed against a population that needs more protein and has less land available, is not a system that scales. It is a system that breaks.

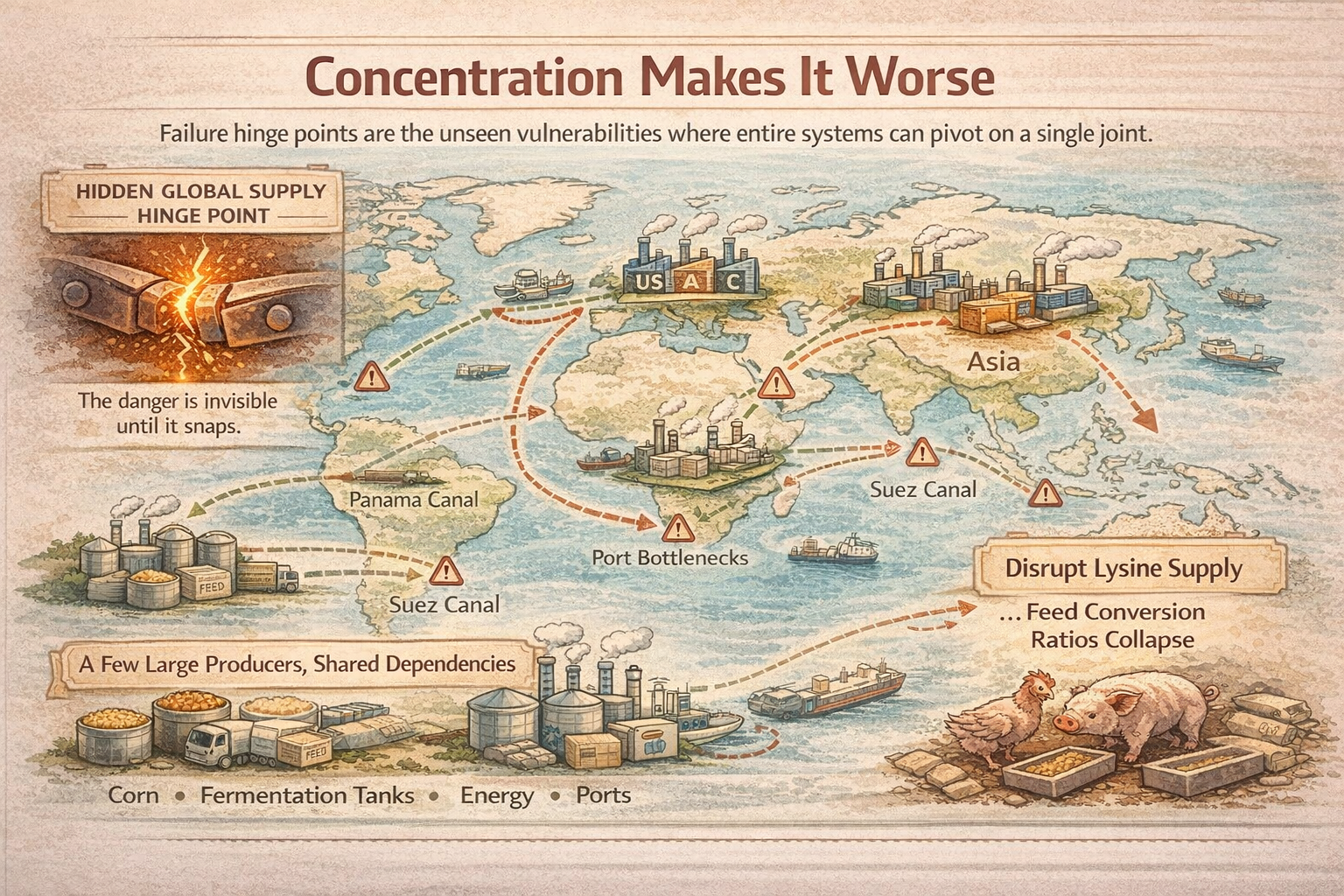

Concentration makes it worse. A useful way to think about this is failure hinge points, the places where the entire system pivots on a single joint. Four countries control the majority of global soy exports. Russia's invasion of Ukraine removed roughly 10% of global wheat supply and 50% of sunflower oil from markets within weeks. But the most dangerous hinge points are invisible until they snap. Industrial amino acids like lysine (added to virtually all commercial animal feed) are produced by a small set of globally scaled fermentation operators; supply is concentrated enough that outages, trade actions, or feedstock shocks ripple quickly through downstream markets.

Soybean crushing capacity, the conversion step that turns raw beans into meal and oil, is bottlenecked in a small number of Midwest facilities. Disrupt that and animal feed prices can spike without a single farm being touched. These are not anomalies. Food and the logistics networks that undergird them are behaving as predicted.

Resilient systems are not built by optimizing a single pathway until it breaks. They are built with redundancy, distributed capacity, and substitution pathways that allow the whole to absorb shocks without cascading into collapse. The internet was designed this way. Power grids are moving this way. Protein infrastructure has not been designed this way at all. A precision fermentation facility can be sited anywhere with reliable power and water, independent of soil chemistry, rainfall, or growing season. Multiple production modes, includingg cropping, bioreactors, abd hybrid systems, mean that when one source fails, others compensate. Resilience is not an afterthought to be retrofitted; it must be embedded in the design from the outset.

Part Two: The Economic Constraint

The protein system we have inherited is not constrained solely by a lack of demand, scientific progress, or entrepreneurial ambition. All of these matter. But the industry has underinvested in the infrastructure required to produce alternative protein at *competitive cost and consistent scale,* and capital over the last decade was often deployed ahead of the systems needed to support it.

Take fermentation-derived proteins as an example. Companies have proven the biology. Perfect Day produces functional whey without a single cow. Meati produces whole-cut steaks and cutlets from mycelium grown through biomass fermentation. Yet in the last few years, both have undergone substantial commercial shifts. Perfect Day pivoted away from direct-to-consumer products toward a B2B model, offering specialized ingredients to food manufacturers. Meati proved consumer demand and product viability, raised hundreds of millions to scale a mega-facility, and then ran into the classic wall: scaling economics and financing structure, ultimately entering a creditor-controlled restructuring.. In both cases, the constraint centered on getting from pilot-scale demonstration to commodity-scale availability. That leap requires commercial bioreactor capacity that has not yet been built at sufficient scale. These facilities cost between $150M–300M, take 3-5 years to finance and construct, and cannot be financed without offtake commitments that most ingredient buyers have not yet been structured to provide.

The result is a deployment gap. The food industry needs to multiply commercial fermentation capacity several-fold by 2035. The investment decisions that determine whether that capacity exists must be made in the next two to four years, before full demand certainty exists. This is not a new problem. It is the same first-of-a-kind infrastructure financing challenge that cloud computing overcame with pay-as-you-go and asset-light operating models, and that semiconductors, industrial gases, and specialty chemicals only scaled through once long-term offtake structures made large capital commitments bankable. In each case, the solution was not better technology. It was better infrastructure logic.

Part Three: The Decarbonization Dividend

Fixing the protein infrastructure problem also addresses one of the largest emissions challenges on the planet, not as the reason to act, but as the consequence of acting.

The land arithmetic alone is striking. Replacing animal-source foods with plant-based or fermentation pathways could reduce agricultural land use by more than 75%, an area equivalent to the combined landmass of the United States, China, the European Union, and Australia. That freed land, if restored, reduces net emissions and over time begins to sequester carbon. The inefficiency problem and the land problem are the same problem.

Methane is the near-term lever. Unlike CO₂, which persists for centuries, methane breaks down in roughly a decade. A ~10% cut in enteric methane is roughly equivalent to eliminating a country the size of Spain’s annual greenhouse gas emissions. That is the single fastest-acting lever available for slowing warming before 2035, and it does not require new energy infrastructure. It requires new protein production infrastructure.

Even so, the alternative protein industry must address common, and legitimate critiques. Commercial-scale protein production is energy intensive, whether in fermentation bioreactors, cultivated meat culture systems, high-moisture extrusion lines, or contract manufacturing facilities. The emissions reduction case depends in part on how that energy is sourced and how efficiently facilities are designed and operated. This is a real engineering challenge the industry has not fully solved consistently, and observers claiming otherwise are getting ahead of the evidence. The path forward is not simple substitution. It is building protein production infrastructure while simultaneously tackling energy intensity as a first-order design problem — the way cloud computing redesigned data centers around massive shared virtualization pools, strict utilization discipline, modular facilities, and long-term power contracts that made efficiency structural rather than optional. The decarbonization dividend is real, but it has to be earned, not assumed.

The Synthesis: Why I Am Here

The three arguments arrive at the same operational conclusion. The protein infrastructure of the next 25 years needs to be built, not incrementally improved, but architected with fundamentally different design choices. Geographic distribution over concentration. Direct conversion over lossy middleware. Commercial structures that make capital-intensive, first-of-a-kind facilities financeable before demand certainty exists.

But infrastructure is not only stainless steel. It is how capacity is defined, replicated, financed, and governed. What is the repeatable unit of scale? Where is failure contained so that a contamination event does not cascade across the system? Which functions are centralized, and which should be regionally distributed? These are design questions as much as engineering ones.

This is where my background becomes relevant. In cloud computing, we learned that capital-intensive systems do not scale through bigger builds alone. They scale through disciplined capacity planning, utilization management, and deployment sequencing. We learned that the right commercial strructures — pay as you go models replacing fixed capital commitments, variable cost structures replacing rigid capacity planning, long-term capacity commitments that let infrastructure investment get ahead of demand — change what is financeable and how fast it gets built. These are not fermentation concepts or food science concepts. They are infrastructure deployment concepts. They have been proven in cloud computing, in semiconductors, in industrial gases, and in specialty chemicals and fragrances. They have not yet been systematically applied to protein production.

Across fermentation, cultivated meat, and plant-based manufacturing, dozens of companies are working to scale novel biomanufacturing platforms. Dedicated facilities require hundreds of millions in capital, multi-year build timelines, long equipment lead times, and complex commissioning, often before demand is fully established. The companies and investors that recognize this moment, and bring infrastructure deployment discipline to it, will define the next decade of protein production.

The goal is not to convince people to eat differently. It is to build a production system where the alternative is available, affordable, and performs the way people expect food to perform. When infrastructure works, choice follows naturally. As we have seen in renewable energy, when a technology reaches cost and performance parity, substitution happens through market logic, not behavior campaigns. The infrastructure made the option real, and adoption followed. Protein production has the same opportunity, not to displace what people love, but to expand what they can choose without compromise.

The central challenge today is not biological discovery alone. The biology is progressing. The question is whether infrastructure models are keeping pace with the ambition placed upon them. The window to shape it is open.

See more at proteinfabric.ghost.io.